2025-03-31 Chris Davis.New York Venture Fund

The average annual total returns for Davis New York Venture Fund’s Class A shares for periods ending March 31, 2025, including a maximum 4.75% sales charge, are: 1 year, 1.39%; 5 years, 15.81%; and 10 years, 9.21%. The performance presented represents past performance and is not a guarantee of future results. Total return assumes reinvestment of dividends and capital gain distributions. Investment return and principal value will vary so that, when redeemed, an investor’s shares may be worth more or less than their original cost. For most recent month-end performance, click here or call 800-279-0279. Current performance may be lower or higher than the performance quoted. The total annual operating expense ratio for Class A shares as of the most recent prospectus was 0.92%. The total annual operating expense ratio may vary in future years. Returns and expenses for other classes of shares will vary.

截至2025年3月31日的各期,Davis New York Venture Fund A类份额在扣除最多4.75%销售费用后的平均年化总回报率为:1年期1.39%;5年期15.81%;10年期9.21%。所示业绩反映过往表现,并不保证未来结果。总回报假设股息和资本利得分配再投资。投资回报和本金价值会有所浮动,因此赎回时,投资者的份额价值可能高于或低于其原始成本。有关最新月末业绩,请点击此处或致电800-279-0279。当前业绩可能低于或高于所引用业绩。根据最近的招募说明书,A类份额的年度总运营费用率为0.92%。未来年度的总运营费用率可能发生变化。其他份额类别的回报和费用将有所不同。

This material includes candid statements and observations regarding investment strategies, individual securities, and economic and market conditions; however, there is no guarantee that these statements, opinions or forecasts will prove to be correct. All fund performance discussed within this material refers to Class A shares without a sales charge and are as of 12/31/24 unless otherwise noted. This is not a recommendation to buy, sell or hold any specific security. Past performance is not a guarantee of future results. The Attractive Growth and Undervalued reference in this material relates to underlying characteristics of the portfolio holdings. There is no guarantee that the Fund performance will be positive as equity markets are volatile and an investor may lose money.

本资料包括有关投资策略、个别证券以及经济与市场状况的坦率陈述和观点;但并不保证这些陈述、观点或预测一定正确。本资料中讨论的所有基金业绩均指不含销售费用的A类份额,数据截至2024年12月31日,另有注明者除外。本资料并非针对任何特定证券的买入、卖出或持有建议。过往业绩并不保证未来结果。本资料中提及的“具有吸引力的增长”和“被低估”均与组合持仓的潜在特征相关。由于股票市场波动,投资者可能会亏损,因此并不保证基金业绩为正。

Performance:

Building Long-Term Wealth

业绩表现:

构建长期财富

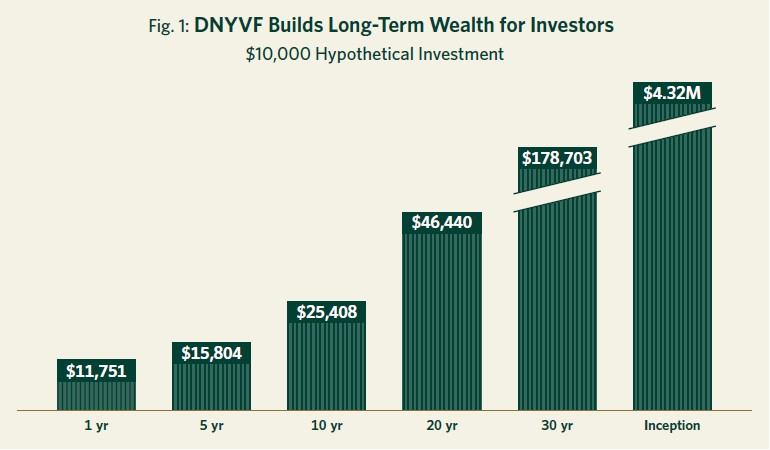

Davis New York Venture Fund (DNYVF) returned +17.51% in the year ended December 31, 2024, and has grown wealth for shareholders in all periods since its inception. The longer a shareholder has been invested in the fund, the more their savings have grown (see Figure 1).

截至2024年12月31日止年度,Davis New York Venture Fund(DNYVF)回报率为+17.51%,自成立以来,各期均为股东创造了财富。投资者在基金中的持有时间越长,其资产增长越显著(见图1)。

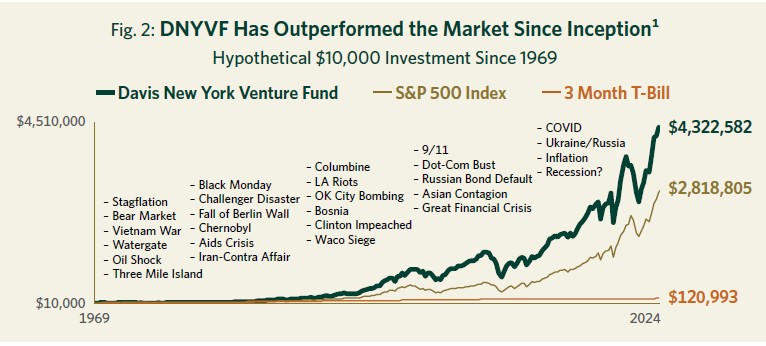

DNVYF results have exceeded the return on the S\&P 500 Index since its inception in 1969. This outperformance, compounded over the fund’s life, means an initial \$10,000 investment made at inception would have grown to \$4,322,582 million by December 31, 2024 (see Figure 2). This is roughly 53% more than if the same \$10,000 had been invested in a passively managed S\&P 500 Index fund over the same period. It is almost 3,500% higher than would have been achieved if the \$10,000 had been held in money market funds for the same length of time.

自1969年成立以来,DNVYF的业绩已超过标普500指数的回报率。这一超额收益在基金生命周期中经复利效应累计,意味着如果在成立之初投资10,000美元,到2024年12月31日,这笔投资的价值将增长至4,322,582美元(见图2)。与同期将同等金额的10,000美元投资于被动管理的标普500指数基金相比,该数值约高出53%;与同期将10,000美元存入货币市场基金相比,则几乎高出3,500%。

Outlook:

Transition and Market Complacency equals Growing Risks and Select Opportunities

展望:

过渡与市场自满意味着风险上升与精选机遇

The economic, technological and geopolitical transitions under way paired with a complacent and concentrated market may lead to greater overall risk and a smaller opportunity set in the years ahead. In this changing environment, our investment discipline is laser-focused on identifying those select, durable and undervalued businesses prepared for transition. As this fast-changing environment unfolds, our fundamental analysis and selectivity are starting to be rewarded while the aggressive risk-taking that rewarded speculators in recent years is becoming more perilous. We are well-positioned for this transition and, after a decade in which our discipline was not rewarded, believe our patience is beginning to pay off.

正在进行中的经济、技术和地缘政治转型,加之市场的自满与集中,可能导致未来几年整体风险加大且机会范围缩小。在这一不断变化的环境中,我们的投资纪律聚焦于识别那些为转型做好准备的精选、稳健且被低估的企业。随着这一快速演变的环境展开,我们的基本面分析与严格筛选开始获得回报,而近年来投机者受益的激进风险行为则变得愈发危险。我们在此次转型中处于有利位置,并且在经历了十年纪律性未获回报后,我们相信耐心正在开始带来回报。

Economic Transition: The End of Free-Money Era

经济转型:零成本资金时代的终结

Beginning with the financial crisis and continuing through March 2022, many of the tenets of sound investing seemed to become irrelevant. In the U.S., interest rate suppression (both directly and indirectly through a bond purchase program known as quantitative easing) accompanied by dramatic increases in government spending and ballooning Federal deficits became a matter of national policy. This was first in response to the Great Financial Crisis of 2008–2009 (GFC) and then to the COVID-19 crisis in 2020–2021.

从金融危机开始并持续到2022年3月,许多稳健投资的原则似乎变得无关紧要。在美国,利率压制(包括直接压制以及通过称为量化宽松的债券购买计划间接压制),伴随着政府支出的大幅增加和联邦预算赤字的激增,成为国家政策。这最初是应对2008–2009年大金融危机(GFC),随后是2020–2021年新冠疫情危机。

As the cost of money approached zero despite huge increases in money supply, these policies created significant market distortions. Assets were mispriced, risks ignored, inflation allowed to metastasize, and valuation discipline penalized. After more than a decade of these distortions, the shift to a more normal environment began in March 2022 when the U.S. Federal Reserve recognized the reality of inflation and announced the first of 11 consecutive increases in the Federal funds benchmark rate. This was the steepest rate of change in the Fed’s history.

尽管货币供应量大幅增加,但资金成本接近零,这些政策造成了显著的市场扭曲。资产被错误定价,风险被忽视,通胀得以蔓延,而估值纪律受到惩罚。在经历了十余年的扭曲后,向更正常环境的转变始于2022年3月,当时美联储认识到通胀的现实,并宣布了11次连续加息中的首次。这是美联储历史上加息幅度最大的一次。

Given the sheer magnitude of the distortions created in the free-money era, the great unwinding that began in 2022 still has a long way to go. Investors should be prepared for unexpected disruptions and heightened volatility. Although the trigger may be unknowable, the high valuations of many of today’s market darlings rest on extremely rosy assumptions which could change quickly should the market’s current optimism be undercut by the unpleasant appearance of one or more so-called black swans, inevitable but unpredictable shocks to the system. As for the short term, we expect that recent interest rate cuts may prove to have been optimistic and that by far the greatest risks investors face today remain from inflation and speculation.

鉴于“免费资金时代”所造成扭曲的巨大规模,始于2022年的“大复位”仍任重道远。投资者应为意外扰动和加剧的波动性做好准备。尽管触发因素可能无法预知,但当今许多市场宠儿的高估值依赖极为乐观的假设,一旦所谓黑天鹅——不可避免却无法预测的系统性冲击——出现,这些假设可能迅速改变。就短期而言,我们预计近期的降息可能过于乐观,而投资者今天面临的最大风险仍然来自通胀和投机。

Technological Transition: AI and Its Implications

技术转型:人工智能及其影响

Technological disruption is also creating significant changes in the investment landscape as investors grapple with the implications of generative artificial intelligence, or so-called GenAI. While we are naturally skeptical of hype, we must begin by stating unequivocally that GenAI is likely to be one of the most transformational technological developments in modern history, and one that is almost certain to create new risks and drive major advances across numerous industries.

技术颠覆同样正在改变投资格局,投资者正在努力应对生成式人工智能(即所谓的GenAI)的影响。虽然我们对炒作保持自然的怀疑,但必须明确指出,GenAI很可能成为现代史上最具变革性的技术发展之一,几乎肯定会带来新风险并推动众多行业的重大进步。

As long-term market observers, we are also equally certain that this revolutionary technology will lead to hyperbole, irrational exuberance2 and unfulfilled promises. The stock market in particular is susceptible to wishful thinking and the fear of missing out (FOMO). FOMO leads investors to pile into companies making the most headline-grabbing claims about the future while turning their backs on those with proven businesses with demonstrated competitive advantages. In particular, we believe many companies are being viewed as, and rewarded as, early beneficiaries of AI demand with the expectation that their revenues and earnings will continue to grow rapidly in the future.

作为长期市场观察者,我们同样坚信,这一革命性技术将引发夸大宣传、非理性繁荣2和无法兑现的承诺。尤其是股票市场易受一厢情愿和“害怕错过”(FOMO)心理的影响。FOMO促使投资者涌入那些对未来做出最耸动宣称的公司,而对那些拥有成熟业务和明显竞争优势的公司却视而不见。我们尤其认为,许多公司正被视为人工智能需求的早期受益者,并因市场预期其收入和盈利将持续快速增长而获得溢价。

The market for AI products and services, however, is still in its early days and competition is fierce. We believe it is very risky to project who the long-term winners and losers will be based on their past one or two years of performance. For example, the substantial technological and societal transformations that the internet heralded in the 1990s culminated in the dot-com bubble and subsequent crash. As our friend Bill Nygren, portfolio manager at Oakmark Funds, recently reminded investors, “in 2000, amidst ‘dot-com’ hysteria, the largest cap Internet companies were Cisco, America Online and Yahoo!. AOL and Yahoo! ended up nearly worthless, and Cisco … has lost 80% relative to the S\&P 500 Index. We think these results should give pause to anyone believing the AI winners have already been determined.”³

然而,AI产品和服务市场仍处于初期阶段,竞争异常激烈。我们认为,仅凭过去一两年的表现来预测长期赢家和输家是非常冒险的。例如,1990年代互联网所引发的重大技术和社会变革最终导致了互联网泡沫及其破裂。正如我们在Oakmark基金的投资组合经理比尔·奈格伦(Bill Nygren)最近提醒投资者的那样:“在2000年‘互联网’狂热之中,市值最大的互联网公司是思科(Cisco)、美国在线(America Online)和雅虎(Yahoo!)。最终AOL和雅虎几乎一文不值,而思科相对于标普500指数已下跌80%……我们认为,这些结果应当让任何认为AI赢家已定的人停下脚步。”³

已经清空了Google。

AI is also likely to prove disruptive to once stable industries in ways that are difficult to anticipate. As one observer recently noted, “when the iPhone was invented, flashlight makers were not worried.” Many companies that have long been considered reliable safe havens or growth darlings are vulnerable to disruption as technology changes business models and consumer behavior. This type of disruption is likely to penalize momentum investors and trend followers who, by definition, assume past trends will continue, as well as risk-averse value investors who may wrongly flock to former safe havens in the service and consumer sectors before realizing that they are as prone to AI disruption as manufacturers once were to globalization. Meanwhile, this disruptive environment may create real opportunities for research-driven investors like us who are willing to be highly selective.

AI也可能以难以预见的方式破坏曾经稳定的行业。正如一位观察者最近所指出的,“当iPhone发明时,手电筒制造商并不担心。”许多长期以来被视为可靠避风港或增长宠儿的公司,随着技术改变商业模式和消费者行为,也变得易受冲击。这类颠覆可能会惩罚那些按定义假设过去趋势将继续的动量投资者和趋势跟随者,也会打击那些风险厌恶的价值投资者——他们可能错误地涌入过去的服务和消费板块避风港,随后才意识到这些领域和制造业曾经面对全球化冲击同样容易受到AI颠覆。与此同时,这一颠覆性环境可能为像我们这样愿意高度精选的研究驱动型投资者创造真正的机会。

Geopolitical Transition: Economic Nationalism and Global Uncertainty

地缘政治转型:经济民族主义与全球不确定性

Geopolitical disruption is the third transition shaping the investment environment as economic nationalism and protectionism replace free trade and globalization. The prospect of higher labor costs, trade wars and increasing global conflict makes characteristics like durability, resiliency and adaptability more important than ever. Our focus on selecting companies that embody these characteristics may well be a tailwind in the decade ahead as investors come to recognize increasing fragility in a period of economic, technological and geopolitical transition.

随着经济民族主义和保护主义取代自由贸易与全球化,地缘政治动荡成为塑造投资环境的第三大转型。更高的劳动力成本、贸易战和日益加剧的全球冲突前景,使得耐久性、韧性和适应性等特征比以往任何时候都更为重要。在经济、技术和地缘政治转型时期,投资者逐渐认识到市场的脆弱性,我们专注于挑选具备上述特征的公司,很可能在未来十年成为我们的顺风优势。

Complacency, Risk and Select Opportunities

自满、风险与精选机遇

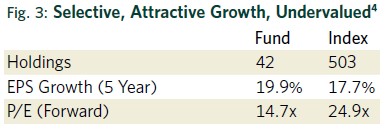

Typically, in an investment environment characterized by transition and uncertainty, markets trade at low valuations. Today, however, this uncertainty has been met with a complacency bordering on denial. Fortunately, in the face of an extremely richly valued and concentrated market, we have put together a very selective portfolio of companies that combine attractive growth with low valuations, a combination we call a value investor’s dream. As shown in Figure 3, our dramatic differentiation from the market allows us to be simultaneously wary of the S\&P 500 Index, which is trading at multiples significantly above the historic average, and optimistic for our selective portfolio of companies which trades at almost a 41% discount to the S\&P 500 Index while actually growing earnings slightly faster.

通常,在一个以转型和不确定性为特征的投资环境中,市场估值偏低。然而,今天这种不确定性却被近乎否认的自满情绪所掩盖。幸运的是,面对一个估值极高且高度集中的市场,我们构建了一个非常精选的投资组合,将吸引性的增长与低估值相结合,这正是我们所谓“价值投资者的梦想”。如图3所示,我们与市场的显著差异,使我们既对以远高于历史均值倍数交易的标普500指数保持警惕,又对我们所精选的略微以更快速度增长盈利、但估值却比标普500指数低近41%的股票组合持乐观态度。

任何时候更保守的持仓都是对的。

Before turning to the details of our portfolio, however, it is worth unpacking the complacency and risk we see in the high valuation and concentration of the indices at today’s levels. Several metrics give a good picture of the risks we see in the averages and the opportunity these risks create for our portfolio.

在深入介绍我们投资组合的具体细节之前,值得先剖析一下我们所看到的指数在当前水平下的高估值与集中度所带来的自满与风险。多个指标清晰展现了我们在平均水平中所看到的风险,以及这些风险为我们的投资组合创造的机会。

Record High Valuations

创纪录的高估值

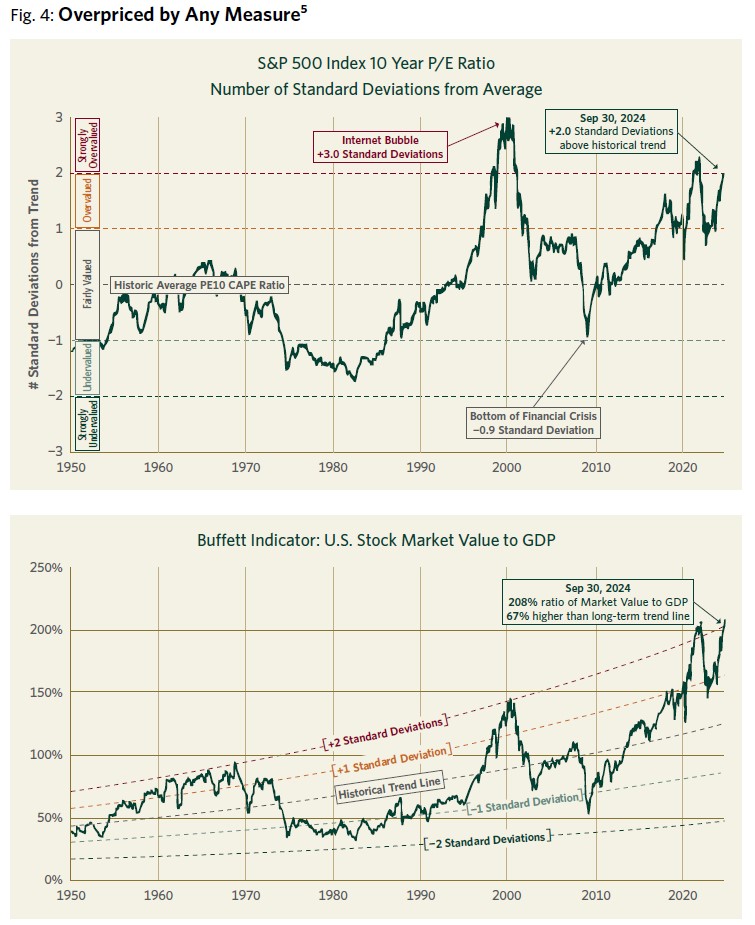

In terms of valuation, as can be seen in Figure 4, the P/E ratio of the S\&P 500 Index is currently around two standard deviations above its historic average. At the same time, U.S. stock market value as a percentage of our total GDP (a ratio often referred to as the “Buffett Indicator” in honor of Warren Buffett who described it as one of the best long-term indicators of the relative attractiveness of stocks) is near its highest level in history.

从估值角度来看,如图4所示,标普500指数的市盈率目前约为其历史均值上方的两个标准差。同时,美国股市总市值占国内生产总值的比重(通常被称为“巴菲特指标”,以纪念沃伦·巴菲特将其誉为衡量股票相对吸引力的最佳长期指标之一)也接近历史最高水平。

Unprecedented Concentration

前所未有的集中度

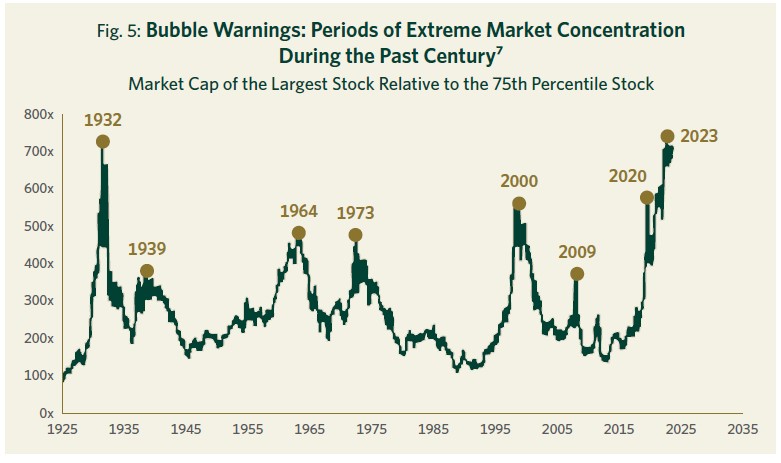

In terms of concentration, a handful of the largest companies represent an unprecedented concentration risk within the richly valued market averages. As shown in Figure 5, such concentration has tended to be a warning sign of a stock market bubble.

在集中度方面,仅少数几家大型公司就代表了估值高企的市场平均水平中前所未有的集中度风险。正如图5所示,这种集中度往往是股市泡沫的预警信号。

过去不代表未来,但保守、本分是应对所有不确定的唯一选择。

Select Opportunities

精选机遇

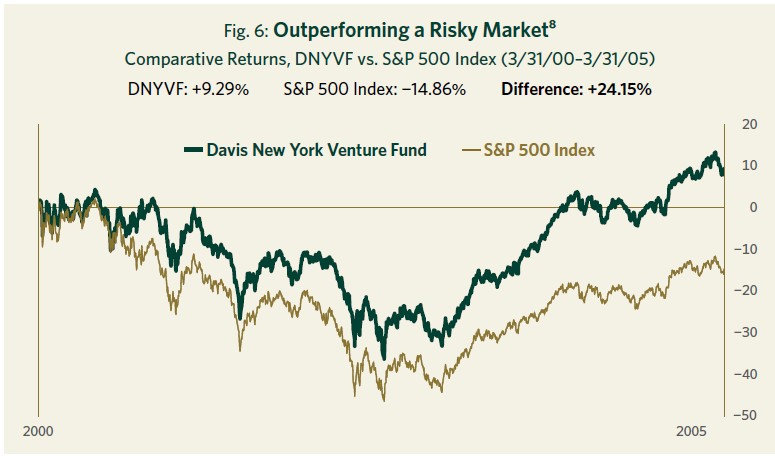

While such bubbles are bad news for index investors, they are often good news for stock pickers. For example, the beginning of the year 2000, much like today, shows up as an extremely overvalued and risky time to invest in the averages. Indeed, as can be seen in Figure 6, in the five years following the March 2000 peak, the total return of the S\&P 500 Index was a negative 14.9%. However, a manager like us who had avoided the siren song of chasing momentum was rewarded for sticking to our discipline with a return of positive 9.3% and relative outperformance versus the S\&P 500 Index of nearly 25 percentage points over this five-year period.6

虽然此类泡沫对指数投资者而言是不利消息,但对个股挑选者而言往往是利好。例如,2000年初,就像今天一样,显示出对平均水平而言是极度高估且风险极高的投资时机。正如图6所示,在2000年3月峰值之后的五年里,标普500指数的总回报率为-14.9%。然而,像我们这样的管理者避免了追逐动量的诱惑,坚持我们的投资纪律,获得了+9.3%的回报,并在此五年期间相对于标普500指数实现了近25个百分点的超额收益。6

Portfolio Positioning:

Selective, Attractive Growth and Undervalued

投资组合定位:

精选、具有吸引力的增长且被低估

Because we have steadfastly adhered to our long-term valuation discipline, the unwinding of the free-money bubble is an overdue but unsettling return to normalcy after more than a decade of delusion. As we return to reality and prepare for more volatile times, we are encouraged that the companies we own (including our carefully selected banks) are well-positioned for this changing environment as investors once again seek durability, profitability, cash production, reasonable valuation and balance sheet strength. These characteristics are becoming increasingly desirable because they allow companies to better navigate a period of transition and uncertainty. While this transition may create headwinds for many of the market darlings that led for so long, it may simultaneously create tailwinds for the type of durable, attractively valued businesses that lie at the heart of our investment discipline, rewarding the patience of our long-term clients.

由于我们始终坚守长期估值纪律,宽松资金泡沫的消退是经历十余年错觉后一个姗姗来迟却又令人不安的回归常态过程。当我们重返现实并为更具波动性的时代做好准备时,我们深感欣慰:我们所持有的公司(包括我们精挑细选的银行)在这一变化环境中均处于有利位置,因为投资者再次追求耐久性、盈利能力、现金创造能力、合理估值和资产负债表稳健性。这些特征正变得愈发受青睐,因为它们使企业能够更好地应对转型与不确定期。尽管此番转型可能为许多长期领先的市场宠儿带来逆风,却也可能同时为那些位于我们投资纪律核心的耐久且估值诱人的企业带来顺风,从而回报我们长期客户的耐心。

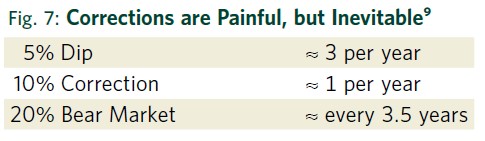

Our conviction includes the recognition that short-term corrections and surprises are an unpleasant but inevitable part of the investment landscape. History shows that investors should expect a 10% correction on average once per year and a 20% correction every 3.5 years (see Figure 7). Given the excesses of the last decade, we see no reason to imagine that the future will be immune from shocks, crises, volatility and corrections. Our job is not to predict the unpredictable but rather to prepare for the inevitable.

我们的信念还包括这样的认识:短期调整和意外虽令人不悦,却是投资环境中不可避免的一部分。历史数据显示,投资者应预期平均每年发生一次10%的调整,每3.5年发生一次20%的调整(见图7)。鉴于过去十年的种种过度现象,我们没有理由认为未来能够免于冲击、危机、波动和调整。我们的职责并非预测不可预测之事,而是为不可避免之事做好准备。

Portfolio Themes and Holdings

投资组合主题与持仓

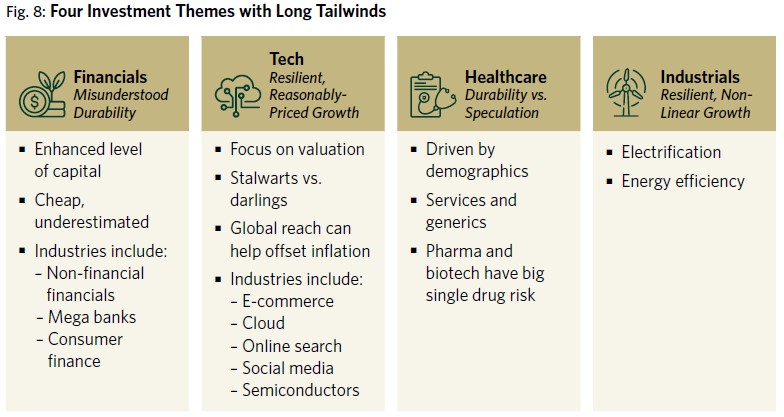

While we build our portfolios from the bottom up based on company-by-company research rather than top-down trends, most of the attractively valued and durable businesses we own reflect four overarching, long-term themes (see Figure 8).

虽然我们构建投资组合是基于逐家公司研究的自底向上方法,而非自上而下的趋势,但我们持有的大多数估值吸引且具有韧性的企业都反映出四个总体的长期主题(见图8)。

Financials: Misunderstood Durability

金融板块:被误解的韧性

Financial companies represent DNYVF’s largest sector weighting and reflect a theme we describe as “Misunderstood Durability.” Since the Great Financial Crisis (GFC), investor sentiment has tended to view financial companies in general and banks in particular as fragile, volatile and prone to disaster. That two large banks (neither of which we ever owned), Silicon Valley Bank and First Republic, collapsed less than two years ago due to company-specific mismanagement reinforced a perception of fragility for all banks. This perception is understandable but inaccurate with regards to the select banks we own, such as Wells Fargo, Capital One and U.S. Bancorp. They actually grew their customer bases through both the GFC and the regional banking crisis of 2023. What’s more, throughout the last decade, a combination of higher capital ratios, larger market shares and tighter regulation have reduced the riskiness of these well-run institutions while increasing their durability and competitive advantages. Their quarterly and even annual earnings can be volatile. However, such “lumpiness” does not diminish the fact that these companies generate capital throughout the business cycle at an attractive rate and use the capital they generate to increase shareholder value by steadily increasing dividends and buying in shares at discounted prices.

金融公司构成了 DNYVF 最大的行业权重,体现了我们所称的“被误解的韧性”主题。自全球金融危机(GFC)以来,投资者普遍将金融公司、尤其是银行视为脆弱、多变且易出险。不到两年前,两家大型银行——硅谷银行和第一共和银行(我们均未持有)因自身管理不善而倒闭,这进一步加深了银行普遍脆弱的印象。对于我们所持有的精选银行(如富国银行、第一资本和美国合众银行)来说,这种观念可以理解但并不准确。这些银行在 GFC 及 2023 年的地区银行业危机期间仍实现了客户基础增长。更重要的是,在过去十年里,更高的资本充足率、更大的市场份额以及更严格的监管减少了这些管理良好机构的风险,同时增强了其耐久性和竞争优势。它们的季度乃至年度盈利可能波动,但这种“坎坷”无损于这样一个事实:这些公司在整个商业周期内以可观速度创造资本,并通过持续提高股息、折价回购股票来提升股东价值。

为什么不是16倍PE(FWD)的AMEX?

Technology: Resilient, Reasonably-Priced Growth

科技板块:韧性强、估值合理的增长

Technology, broadly defined, makes up the portfolio’s next largest theme. As with financials, the term technology covers a broad range of companies with diverse types of business models. Within the tech universe, we focus on a select few companies that combine proven long-term growth with reasonable valuations. This valuation discipline has led us to avoid many of the market darlings that have driven the S\&P 500 Index in recent years, including the majority of the so-called Magnificent Seven tech darlings that today represent a concentration of over 33% of the S\&P 500 Index.¹⁰

从广义上看,科技板块构成了组合中的第二大主题。与金融板块类似,“科技”涵盖了商业模式多样的广泛企业。在这一领域,我们专注于少数兼具长期增长记录与合理估值的公司。正是这种估值纪律,使我们避开了许多近年来推动标普 500 指数上涨的市场宠儿,包括如今占标普 500 指数权重逾 33% 的所谓“七巨头”中的大部分公司。¹⁰

In fact, while others have been piling into companies like Meta and Alphabet which we have owned for many years, we have used their outperformance in recent years as an opportunity to reduce our positions in these excellent, but richly valued, companies. Although we now own fewer shares, the strong business models and proven managements of these companies (along with Amazon) have still earned them a place in our portfolio. In addition, instead of market darlings such as Nvidia, Apple or Tesla, our remaining technology investments have been focused in durable, proven but less glamorous parts of the technology sector such as semiconductor manufacturing (Texas Instruments and Samsung) and capital equipment (Applied Materials).

事实上,当其他投资者蜂拥买入我们已持有多年的 Meta 和 Alphabet 等公司时,我们利用其近年来的优异表现减少了对这些优质但估值高企公司的持仓。虽然目前持股较少,但这些公司(以及亚马逊)稳健的商业模式和成熟的管理团队仍使其保留在我们的投资组合中。此外,我们并未投资 Nvidia、Apple 或 Tesla 等市场明星,而是将剩余的科技持仓集中在科技领域中更为耐久、经过验证但不那么耀眼的领域,如半导体制造(德州仪器、三星)和半导体设备(应用材料)。

As we discussed earlier, all investments (not just those in the technology sector) are likely to be affected by the much heralded breakthroughs in artificial intelligence. In preparing for this impact, investors should bear in mind Roy Amara’s famous law that we “overestimate the effect of a technology in the short run and underestimate the effect in the long run.”¹¹ As with the internet, our approach is to avoid the “story stocks” and instead ask which companies can use this powerful new tool most effectively to build the value of their businesses and, just as importantly, which companies are most threatened by the new technology. While AI stocks will likely go through booms and busts, the underlying technology is transformative and seems certain to be a permanent part of the economic landscape going forward. As such, questions about its impact are already a standard part of our research process.

正如前文所述,所有投资(不仅仅是科技板块)都可能受到备受关注的人工智能突破的影响。为应对此影响,投资者应牢记罗伊·阿马拉的著名定律:“我们高估一项技术的短期影响,却低估其长期影响。”¹¹ 与互联网类似,我们的做法是回避“故事股”,转而思考哪些公司能最有效地利用这一强大的新工具来提升企业价值,并同样重要的是,哪些公司最有可能受到这一新技术的威胁。虽然 AI 概念股可能经历繁荣与萧条,但 AI 技术本身具有变革性,未来必将成为经济格局的永久组成部分。因此,关于其影响的问题已成为我们研究流程的标准环节。

Healthcare: Durability vs. Speculation

医疗保健:耐久性与投机性

For decades, healthcare spending relentlessly rose from 5% of U.S. GDP in 1960 to roughly 17% in 2010. However, reflecting the wisdom of Herb Stein’s famous observation that “if something cannot go on forever, it will stop,” the rollout of the Affordable Care Act in 2010, along with a range of other public and private initiatives, has led to a flattening of this growth since then. Today, while healthcare spending remains a political hot button, it is somewhat encouraging that 15 years later, its percentage of GDP still stands at 17% despite the invention of many expensive new therapies in the interim.

几十年来,美国医疗保健支出从1960年占GDP的5%持续上升到2010年的约17%。然而,正如赫伯·斯坦著名的箴言所言,“如果一件事无法永远持续,它就会停止”,2010年《平价医疗法案》的推出以及众多公共和私营领域举措的实施,使这一增长曲线趋于平缓。如今,尽管医疗支出依旧是政治热点话题,但令人稍感宽慰的是,15年过去,尽管期间发明了许多昂贵的新疗法,医疗支出占GDP的比例仍保持在17%。

To offset the rising costs of novel treatments and innovative (and patented) pharmaceutical therapies, the healthcare system has needed to constantly find savings elsewhere. As a result, our investments in this important sector have focused on those companies that play a part in moderating or reducing the natural rate of increase in healthcare spending. Companies such as Cigna and Humana, for example, offer programs like Medicare Advantage which deliver patients a higher quality of care at a lower cost. Given the inefficiencies and incentives of government agencies versus the private sector, we are not surprised that such companies have long records of success. Similarly, lab-testing companies like Quest Diagnostics and branded generics companies like Viatris continue to reduce costs in the healthcare system. On the other side of the ledger, while we marvel at the enormous profits created by novel pharmaceutical and biotech breakthroughs, we find it difficult and risky to try to predict the next winners while also quantifying the duration of those profits given the development of me-too competitors and evolving drug reimbursement policies.

为了抵消新疗法及创新(且受专利保护)药物治疗成本的上升,医疗体系必须不断在其他方面寻找节省空间。因此,我们在这一重要领域的投资聚焦于那些能够减缓或降低医疗支出自然增速的公司。例如,信诺(Cigna)和 Humana 等公司推出 Medicare Advantage 等项目,以更低成本为患者提供更高质量的护理。考虑到政府机构与私营部门在效率和激励机制上的差异,这类公司长期以来的成功轨迹并不令人意外。同样,Quest Diagnostics 这类实验室检测公司和 Viatris 这类品牌仿制药企业也在持续为医疗体系降本。另一方面,尽管我们对新药和生物技术突破所创造的巨额利润叹为观止,但考虑到“跟随”竞争者的出现及药物报销政策的变化,预测下一批赢家并量化其利润持续期既困难又风险高。

Industrials: Resilient, Non-Linear Growth

工业板块:韧性强、非线性增长

In an age of digitization, software, AI, content creation, advertising and hot consumer brands, companies that operate railroads and generate electricity (Berkshire Hathaway), extract copper (Teck Resources), manufacture insulation (Owens Corning), supply food (Tyson) or produce oil (Tourmaline Oil) may sound dull, but our civilization cannot function without their products. The necessity of these products and, in many cases, the environmental risks of producing them, create regulatory and legal complexity. Their production often requires large upfront capital investment. In any short-term period, their demand and supply may be subject to cyclical swings, resulting in earnings volatility for producers. Further, as such products are not especially differentiated, price and availability are often the only drivers of customer preference, making it difficult for any one company to maintain high returns without attracting new competition.

在数字化、软件、AI、内容创作、广告和热门消费品牌盛行的时代,经营铁路和发电(伯克希尔哈撒韦)、开采铜矿(泰克资源)、生产保温材料(欧文斯科宁)、供应食品(泰森)或开采石油(Tourmaline Oil)等企业听起来或许乏味,但没有它们的产品,现代文明将无法运转。这些产品的必要性以及在许多情况下其生产所伴随的环境风险,带来了监管和法律的复杂性。其生产往往需要巨额前期资本投入。在任何短期阶段,其供需都可能出现周期性波动,导致生产商盈利波动。此外,由于此类产品差异化不大,价格和可获得性通常是客户偏好的唯一驱动因素,这使得任何公司都难以在不吸引新竞争者的情况下维持高回报。

So how do we find attractive opportunities in such a difficult category? First, because many such dull businesses are overlooked and out of favor in today’s growth-driven market, carefully selected industrials currently sell at extremely low valuations. This is despite their having long-term records of growth, durable earnings power, and competitive advantages driven by low-cost assets or economies of scale, and some inflation protection due to long-lived assets. What’s more, certain long-term trends may be accelerating the growth rates of a number of these companies. For example, in a world of massively expanding computing power, the need for electricity is markedly accelerating. Also, trends like electrification of automobiles and expansion of the electricity grid increase copper demand at a rate that is likely to continue to outstrip growth in supply (a byproduct of the enormous regulatory challenges of permitting and building new mines).

那么,我们如何在如此艰难的类别中寻找有吸引力的机会?首先,由于这些“乏味”企业在当今由增长驱动的市场中常被忽视且不受青睐,经精挑细选的工业公司目前市值处于极低水平。尽管它们拥有长期增长记录、持久盈利能力、依托低成本资产或规模经济构建的竞争优势,并因长期资产而具有一定抗通胀能力。更重要的是,一些长期趋势可能正在加速其中部分企业的增长。例如,在计算能力大幅扩张的世界里,对电力的需求正在显著加速;此外,汽车电动化和电网扩张等趋势使铜需求以可能持续超过供给增长的速度增长(这是受新矿许可与建设监管挑战巨大所驱动的结果)。

Finally, in ways that are hard to anticipate, the advent of AI discussed earlier is almost certain to create enormous disruptions in many white-collar service industries in much the same way that automation and globalization impacted U.S. manufacturing industries and blue collar workers in the 1980s and 1990s. As the services sector faces significant uncertainty in the years ahead, people may be more enthusiastic about our industrial holdings with their low valuations, dull business models and resistance to obsolescence.

最后,如前所述,AI 的出现几乎可以肯定会以难以预料的方式对许多白领服务行业产生巨大冲击,正如自动化和全球化在20世纪80年代和90年代对美国制造业及蓝领工人产生的影响一样。随着服务业在未来几年面临重大不确定性,市场可能会对我们那些估值低廉、商业模式“乏味”且不易被淘汰的工业持仓表现出更高热情。

Looking Ahead:

展望未来:

A Turning Tide

潮流正在转向

After a long stretch in which our investment discipline was out of favor, we see many indications that the tide is turning. The current combination of economic, technological and geopolitical transitions bodes poorly for momentum/trend-following investors, while high market valuations and extreme concentration bode poorly for the major stock indices and passive investors. In contrast, our highly selective approach and proven long-term investment discipline is becoming more important than ever.

在我们遵循的投资纪律长期不受青睐之后,我们看到许多迹象表明形势正在发生逆转。当前经济、技术和地缘政治的多重转型对动量/趋势跟随型投资者不利,而高市场估值和高度集中度则对主要股票指数和被动投资者不利。相反,我们高度精选的方法和久经考验的长期投资纪律正变得比以往任何时候都更加重要。

While we expect periods of volatility and disruption as we move out of the era of free-money and cheap capital, the combination of above-average growth and below-average valuations that characterizes our portfolio today is rare. It positions us well to reward investors who resisted the bandwagon’s siren song and held fast to our patient, long-term approach to building generational wealth. The key pillars of success in this tumultuous environment are the cornerstones of our investment discipline, based on what we look for in our portfolio companies: cash generation, conservative capital structure, durable business model, low valuation and proven management.

随着我们走出零成本资本时代,我们预计将经历波动和动荡期,但我们当前投资组合所呈现的高于平均水平的增长与低于平均水平的估值这一组合极为罕见。这使我们能够回报那些抵制随波逐流、坚持耐心长期积累世代财富的投资者。在这一动荡环境中取得成功的关键支柱,正是我们投资纪律的基石:现金创造能力、保守的资本结构、稳健的商业模式、低估值以及成熟可靠的管理团队。

For more than 50 years we have navigated a constantly changing investment landscape guided by one North Star: to grow the value of the funds entrusted to us. We are pleased to have achieved strong results thus far and look forward to the decades ahead. With more than \$2 billion of our own money invested in our portfolios, we stand shoulder to shoulder with our clients on this long journey.12 We are grateful for your trust and are well-positioned for the future.

五十多年来,我们在不断变化的投资环境中航行,始终以一个北极星为指引:提升受托基金的价值。我们很高兴迄今取得了优异成绩,并期待未来几十年的发展。我们在自有投资组合中投资逾20亿美元,与客户并肩踏上这段漫长旅程。12 我们感谢您的信任,并已为未来做好充分准备。

热门主题

Recent Articles

2026-04-04 Andrej Karpathy.LLM Wiki

Refer To:《2026-04-04 Andrej Karpathy.LLM Wiki》。 LLM Wiki A pattern for building personal knowledge bases using LLMs. 一种使用 LLM 构建个人知识库的模式。 This is an idea file, it is designed to be copy pasted to your own LLM Agent (e.g. OpenAI Codex, Claude Code, ...2026-04-28 潘乱.从红果到AI短剧:谁在革谁的命?

Refer To:《从红果到AI短剧:谁在革谁的命?》。 红果短剧的快速崛起与用户增长逻辑 红果短剧在三年内实现日活过亿的爆发式增长,主要得益于其免费模式和对非长视频用户的有效触达。与优爱腾等长视频平台偏向正剧的定位不同,短剧更接近于电影的消费体验,但通过广告变现降低了消费门槛。AI 漫剧作为新兴品类,在去年下半年开始崭露头角,虽然与传统大制作动漫路径不同,但其生产效率和题材丰富度正在迅速提升,成为行业新的增长点。 王小书: (00:04) Hmm. 潘乱: (00:04) ...2020-12-10 王宁.潮流玩具风靡背后的心理学

Refer To:《泡泡玛特王宁:潮流玩具风靡背后的心理学》。 于近年来以Molly、Pucky、Dimoo等各类IP受到Z世代消费者欢迎的泡泡玛特,其实已经有十年历史。 “我从自己刷墙,开第一家实体店,做零售业,是在2008年5月13号,到这周末就是整整11年了。我们是创业老兵了,单泡泡玛特这个品牌就有9年。” ...2022-01-08 王宁.不做「你死我活」的生意

Refer To:《泡泡玛特王宁:不做「你死我活」的生意》。 今年全球最火的玩具,非Labubu莫属。 6月11日,一只稀有款薄荷色Labubu以人民币108万元成交价在二级市场拍出。就是下面这只—— 图片 6月14日,因为韩国地区线下销售太火爆,恐引发安全问题,泡泡玛特发公告暂停Labubu全系列销售。 Labubu全球爆火直接拉动泡泡玛特股价飙涨,今年以来,其股价涨幅超过200%,市值超过3500亿元,创始人王宁也因此取代牧原股份秦英林,成为新晋河南首富。 ...2026-05-13 Alex Wang.Meta's AI Chief On AI Beef, New Models And Life With Zuck

Refer To:《Meta's AI Chief On AI Beef, New Models And Life With Zuck》。 Meta Superintelligence Labs Structure and Strategic Compute Advantage Meta Superintelligence Labs 的组织结构与战略算力优势 Meta Superintelligence Labs (MSL) operates through a specialized ...